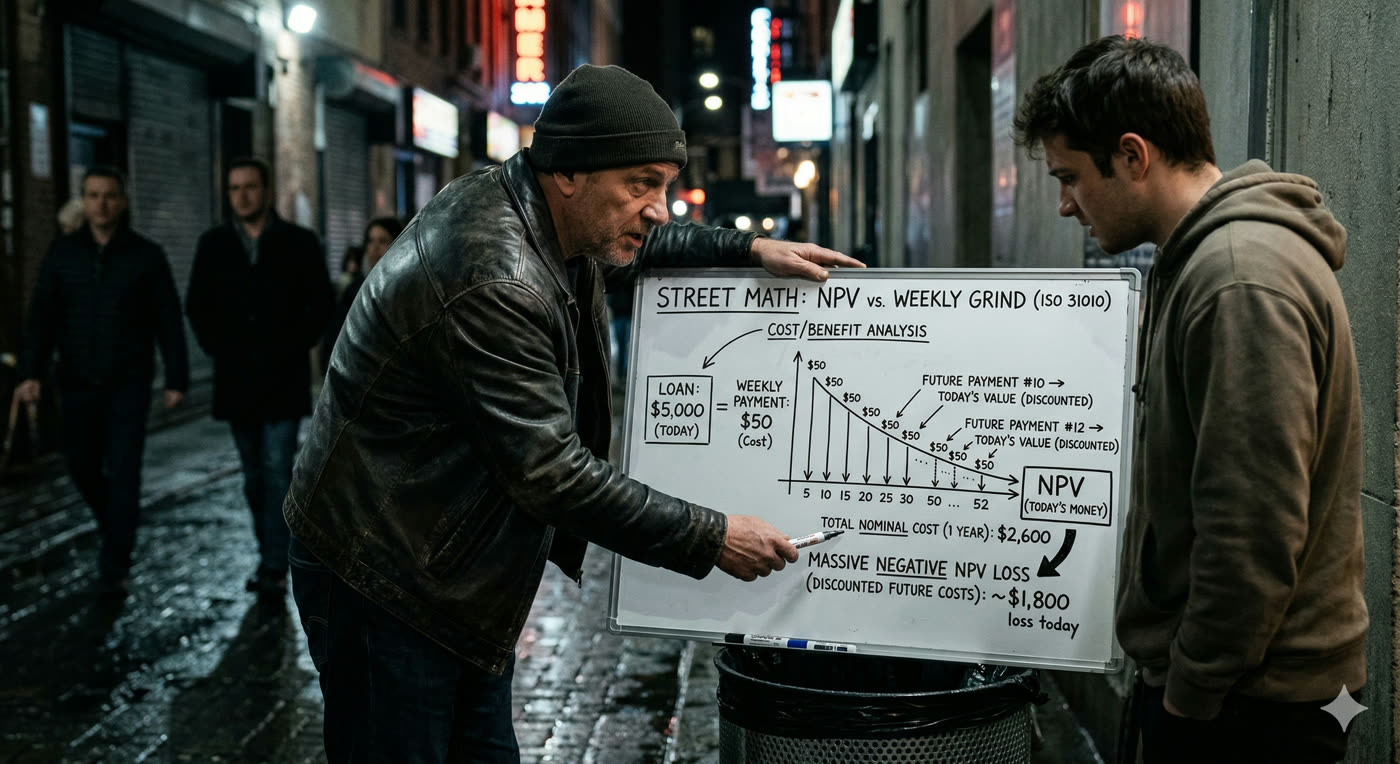

THE LOAN: $1,000 today → $50/week interest

Payback at week 26: principal + accumulated

DISCOUNT RATE: 15%/year ≈ 0.29%/week

NPV (borrower's perspective):

┌─────────────────────────────────────────────┐

│ NPV = +$1,000 │

│ - Σ[ $50 / (1.0029)^n ] for n=1..26 │

│ - $1,000 / (1.0029)^26 │

│ │

│ Discounted payments ≈ $1,270 │

│ Discounted principal ≈ $927 │

│ Total present cost = $2,197 │

│ │

│ NPV = $1,000 - $2,197 = -$1,197 ✗ │

└─────────────────────────────────────────────┘

EFFECTIVE ANNUAL RATE:

$50/wk on $1,000 = 5%/week → (1.05)^52 - 1 ≈ 1,164%

Every dollar borrowed destroys $1.20 in value.

FADE IN: A cluttered pawn shop office. Gold chains in glass cases. A desk calculator from the 1980s. LEON (50s, calm, well-dressed for a pawn shop, speaks softly because he doesn't need to yell) sits behind the desk. CARLOS (30s, desperate, fidgeting, needs money yesterday) sits across from him. CARLOS I need a thousand. I can pay you back fifty a week. That's fair, right? LEON (leaning back) Fifty a week. Let me ask you something, Carlos. Do you know what that fifty dollars actually costs you? CARLOS It costs fifty dollars. That's the point. LEON (smiling) No. That's the illusion. The fifty dollars you pay me next week is not the same as the fifty dollars you pay me in six months. And until you understand why, you're going to keep sitting in that chair.

Leon opens a desk drawer and pulls out a crisp hundred-dollar bill. He holds it up. LEON This hundred dollars today — what's it worth? CARLOS A hundred dollars. LEON Wrong. It's worth MORE than a hundred dollars. Because if you have it today, you can use it today. Invest it, spend it, earn with it. A hundred dollars in your hand right now is worth more than a hundred dollars promised to you a year from now. CARLOS Why? LEON Three reasons. Inflation: prices go up, so future dollars buy less. Opportunity cost: money today can be put to work earning more money. And risk: the future is uncertain — that promised hundred might never arrive. He sets the bill down. LEON (CONT'D) This is called the Time Value of Money. It's the foundation of every financial calculation that matters. And it's the reason your "fifty a week" is not what you think it is.

LEON To compare money at different points in time, you need a Discount Rate. Think of it as the cost of waiting. The higher the rate, the less future money is worth today. He pulls out the calculator. LEON (CONT'D) A bank might use 5% per year. A venture capitalist might use 20%. For someone in your situation — high risk, no collateral, urgent need — the effective discount rate is much higher. Let's say 15% per year, or about 0.29% per week. CARLOS That doesn't sound like much. LEON It doesn't SOUND like much. But it compounds. Every week, the value of your future payment shrinks a little more. The fifty dollars you pay me in week one is worth about $49.85 in today's money. The fifty you pay in week twenty is worth about $47.20. The fifty you pay in week forty? About $44.70. CARLOS So the same fifty dollars is worth less and less? LEON To ME, yes. But to YOU, it costs the same effort every single week. That's the asymmetry I profit from.

LEON Now let's calculate the Net Present Value of your deal. NPV is the sum of all future cash flows, each one discounted back to today's value. He starts punching numbers. LEON (CONT'D) You want a thousand dollars today. You'll pay me fifty a week for... how long? CARLOS Until it's paid off. Twenty weeks? LEON (laughing softly) Twenty weeks at fifty is a thousand. That's just the principal. My fee is fifty a week in INTEREST. The principal stays. You pay fifty a week until you can pay back the full thousand PLUS the weekly fifty. CARLOS (paling) So I'm paying fifty a week... forever? LEON Not forever. But let's say it takes you six months — 26 weeks — to save up the thousand to pay me back. In that time, you've paid me 26 times fifty: $1,300 in interest. Plus the $1,000 principal. Total: $2,300 for a $1,000 loan.

LEON Let me show you the NPV from YOUR perspective. You receive $1,000 today. That's positive. Then you pay $50 per week for 26 weeks, plus $1,000 at week 26. All negative. He writes: LEON (V.O.) NPV = +$1,000 - Σ($50 / (1 + 0.0029)^n) for n=1 to 26 - $1,000/(1.0029)^26 LEON (CONT'D) The discounted value of the 26 weekly payments is about $1,270. The discounted value of the final $1,000 payback is about $927. Total present value of what you pay: $2,197. He circles the result. LEON (CONT'D) NPV for you: $1,000 minus $2,197 equals NEGATIVE $1,197. You're destroying $1,197 in present value. For every dollar I lend you, you lose a dollar twenty in real terms. CARLOS (staring at the numbers) That can't be right. LEON It's exactly right. The fifty a week FEELS small. But when you discount all those payments back to today and add them up, the true cost is more than double the loan.

LEON Want to know your effective annual interest rate? Fifty dollars a week on a thousand-dollar principal. That's 5% per WEEK. CARLOS Five percent doesn't sound bad. LEON Per WEEK. Compounded. The effective annual rate is: (1.05)^52 minus 1. He calculates. LEON (CONT'D) That's 11.6. As in 1,160%. Your annual interest rate is over a thousand percent. CARLOS (standing up) That's insane. LEON (calmly) Sit down. I'm not trying to sell you the loan. I'm trying to show you the math so you can make an informed decision. Most people in your position don't see these numbers. They see "fifty a week" and think it's manageable. The math says otherwise. Carlos sits back down, slowly.

LEON Let's do a proper Cost/Benefit Analysis. What do you need the thousand for? CARLOS My car's transmission. Without it, I can't get to work. I lose my job. LEON Now we have a benefit to quantify. What do you earn? CARLOS Six-fifty a week, take-home. LEON So the benefit of the loan is: you keep your job. The value of that over 26 weeks is 26 times $650 equals $16,900 in income preserved. He writes two columns: LEON (V.O.) BENEFITS: - Income preserved: $16,900 - Continued employment: ongoing value COSTS: - Interest payments: $1,300 - Principal repayment: $1,000 - NPV of total payments: $2,197 - Opportunity cost of $50/week: reduced savings capacity LEON (CONT'D) Net benefit: $16,900 minus $2,300 equals $14,600. The loan is a terrible financial product but a rational economic decision — IF and ONLY IF losing the car means losing the job.

LEON But a good CBA doesn't stop at one option. You compare alternatives. He adds columns: LEON (CONT'D) Alternative one: Borrow from me. Cost: $2,300. Benefit: keep job. Net: +$14,600. Alternative two: Ask your employer for a $1,000 advance. Cost: maybe $0 in interest, but social cost — you look desperate. Probability they say yes: maybe 40%. Alternative three: Use public transit for a month while you save. Cost: $120 in bus passes plus 90 extra minutes commuting daily. Risk: 15% chance of being late enough to get fired. Alternative four: Find a credit union emergency loan. Cost: maybe $1,100 total at 18% APR. But processing takes two weeks — can you survive two weeks without the car? CARLOS I didn't think about the credit union. LEON Most people don't. They see the immediate problem and grab the immediate solution. CBA forces you to line up ALL the options and compare them on the same basis — Net Present Value.

Leon draws a comparison table. LEON (V.O.) Option | NPV Cost | Probability | Risk-Adjusted NPV Loan from me | -$2,197 | 100% | -$2,197 Employer advance| -$0 | 40% | -$0 (but 60% chance of plan B) Public transit | -$350 | 85% success | -$298 (15% job loss risk = -$2,535) Credit union | -$1,050 | 90% | -$945 (10% timing risk) LEON (CONT'D) Risk-adjusted, the credit union loan costs you $945 in present value. My loan costs you $2,197. The credit union is less than half the cost. CARLOS But it takes two weeks. LEON So the real question is: can you survive two weeks? If yes, the credit union saves you $1,252 in present value. If no, my loan is the rational choice despite being expensive. The CBA doesn't tell you what to WANT. It tells you what each option actually COSTS. CARLOS (thinking hard) My brother could drive me for two weeks. LEON Then you just found a bridge strategy that makes the credit union option viable. Your effective cost just dropped from $2,197 to about $945 plus whatever you owe your brother in gas money.

Carlos stands up. He hasn't taken the loan. CARLOS I'm gonna try the credit union first. LEON (nodding) Smart. And if they say no, I'm still here. Same terms. I don't change the price based on desperation — that's a different kind of business. He walks Carlos to the door. LEON (CONT'D) ISO 31010, Section B.9.2. Cost/Benefit Analysis and Net Present Value. Governments use it to decide whether to build highways. Hospitals use it to evaluate new equipment. You just used it to avoid a thousand-percent interest rate. CARLOS Why'd you show me all that? You could've just given me the loan. LEON (leaning against the doorframe) Because an informed borrower is a borrower who pays me back. And a borrower who understands NPV? He only comes to me when he truly has no other option. That's the customer I want — the one who's done the math and decided I'm still the best choice. Not the one who's just desperate. Carlos nods and walks out into the night. Leon watches him go, then returns to his desk and his calculator. FADE OUT. — END —